Energy Cable: The rollercoaster in crude oil continues

Energy Cable: The rollercoaster in crude oil continues

Last week we were close to writing our obituary on our crude oil long position and this week we are almost back in green. The last few weeks in crude have surely been something!

Excerpt: The crude market is rife with subtle tit-for-tat politics, and there's little to indicate this dynamic will change. We delve into the current state of the oil market and share our thoughts on our current position at this stage.

First we broke USD 80, then Al Jazeera reported a ceasefire between Israel and Palestine, which was retracted 15 min later. The market didn’t care and pounded the sell-bottom all the way back below 78 even with (on the paper) strong jobs and PMI prints out of the US coming out in the meantime. Now it seems like the market has woken up and smelled the coffee, let’s see how long it lasts this time. We remained in long crude and luckily didn’t get stopped out last week.

Chart 1: You just have to moan enough for crude to get >80 again

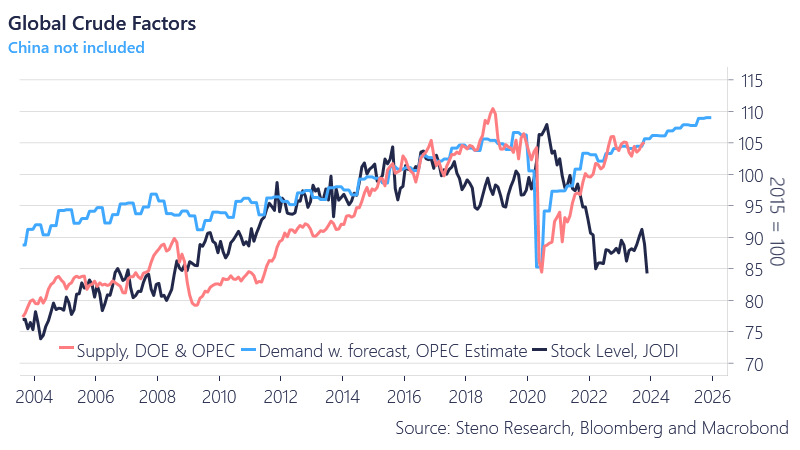

Last week we noted that geopolitics and strong US economic data should see crude oil trading higher while a stronger DXY plays a part in weakening crude. This week we got data from the supply side to support our long conviction. Firstly, looking at the below chart we note that global stock levels excluding China are 15% lower than 2015 while both supply and demand are 5% higher.

With stock levels this weak compared to supply and demand, it means a greater impact on price. On the supply side we note that OPEC looks to continue its expected cuts with Iraq indicating its willingness to comply.

In the below chart we have excluded China since Chinese stock data is non-existent. Perhaps distillate stock levels in Singapore, a large exporter towards China, could be a hint that stock levels in China are low as well.

Apart from the impact of low stock levels we note the impact from Indian buying of cheap Russian crude oil. The minister of oil in India, Sri Jegarajah, said that “If we start buying more Middle Eastern oil, the oil price will not be at $75 or $76. It will be $150”. A more direct yet subtle rejection of Iraq's latest commitments could hardly be imagined, but in a broader context, it likely serves as a rebuff to the recent efforts of OPEC as a whole. The gradual increase in Urals crude imports by India is subtly undermining OPEC's supply dominance, stretching the coffers on Middle Eastern Producers.

The geopolitical discount on Russian crude has, of course, been highly beneficial to the energy bills of India (and let's not overlook China), but the recent shift in Ukrainian strategy to target Russian oil infrastructure and refineries should raise concerns for major importers.

This situation is especially critical given that global stock levels are depleted, currently approximately 15% below the levels of 2015. The drainage of the Strategic Petroleum Reserve (SPR) in the US is also contributing to this emerging fragility

Chart 2.a: Demand, supply and stock numbers globally ex. China

Keep reading with a 7-day free trial

Subscribe to The Energy Cable to keep reading this post and get 7 days of free access to the full post archives.