Energy Cable #58: MASSIVE bottlenecks and abundances in shipping and energy space

Energy Cable #58: MASSIVE bottlenecks and abundances in shipping and energy space

Nat Gas levels are far below sector break-evens, making it a tug of war between short-sellers and producers. Nat Gas looks like a bargain, but let’s see whether the chicken comes home to roost.

In sum:

- Price benchmarks of Nat Gas among major producers have fallen off a cliff relative to price benchmarks of major net consumers/importers as the halt to global shipping has led to regional bottlenecks and abundances.

- We remain long US Nat Gas as a minor improvement in shipping paired with bottlenecks in 1-2 months from now makes for a potential extremely bullish cocktail if it squeezes out the current aggressive short-selling by CTAs.

- We expect a spill-over from shipping to the pricing of goods -and commodities in maximum 1-2 months from now as the demand side price benchmarks are currently physically overloaded, which will not be the case once the lag-effects of a complete freeze of global shipping kick in.

Hello from a sunny but chilly Copenhagen.

Since we haven't talked about shipping in a couple of weeks, we thought that we would do an update on what currently looks like an overextended market searching for a new equilibrium. The shipping rates may have plateaued at elevated levels, but now is the time where spill-overs are starting to show up in physical goods and commodities.

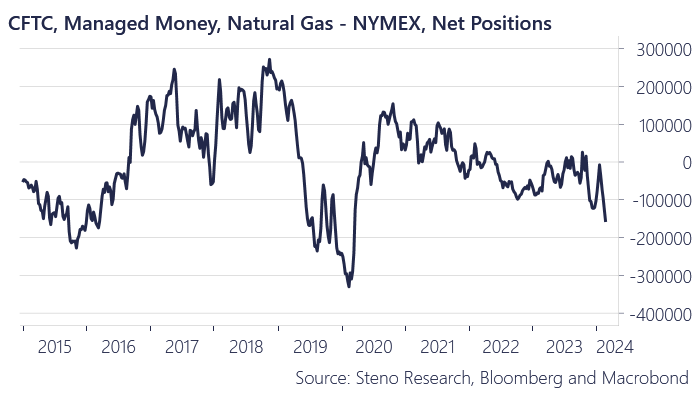

We entered a highly contrarian long position in Nat Gas last week among other things due to technicals and a stretched positioning, but also due to the spill-overs from shipping. Last week, net positioning reached lows not seen since peak lockdowns leading prices below sector break-evens. This is likely going to lead to an OPEC versus paper market style game of chicken between producers and CTAs, with a large correction possible if short-sellers blink first

We expected a bumpy ride, when we entered and the volatility has not failed to deliver, but we are so far in the money on the trade. The massive freeze in global shipping is worth tracking here as the current supply side abundances is likely a symptom of future demand side scarcities.

Read long why below..

Chart 1: Ultra short positioning i natural gas

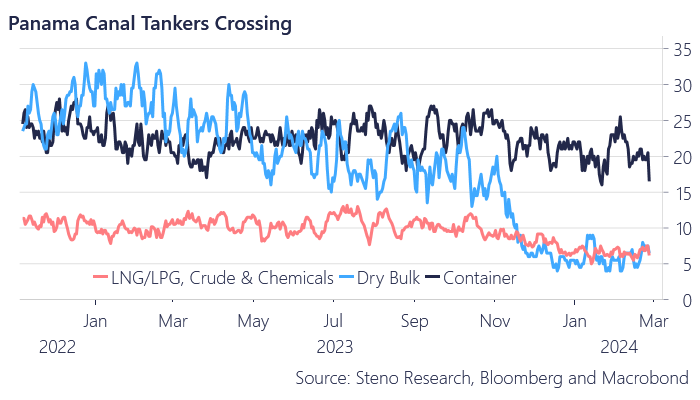

The supply side distortions stemming from issues in both the Panama- and the Suez canal will soon be felt across the goods- and commodity landscapes.

Crossings remain historically low and we are running at low levels across dry bulk, LNG/LPG and Crude and there are no major signs of improvement.

Had we seen a different weather situation, this would have turned into a massive bottle-neck headache for those on the receiving end of the flows, while this has now instead turned into a headache for those on the distributing end of the equation as LNG flows have stranded at the producing end in both the Middle East and the US (read Qatar and the US).

Poten LNG prices from Australia and Qatar have diverged accordingly, which is a sign that the lack of shipping accessibility/feasibility (from Qatar to Europe) is an issue for the producer rather than the consumer for now. This balance is likely starting to TURN during the early innings of the spring.

Chart 2a: Panama crossings

Chart 2b: Suez crossings

Keep reading with a 7-day free trial

Subscribe to The Energy Cable to keep reading this post and get 7 days of free access to the full post archives.